Understanding Student Loan Consolidation

In the pursuit of higher education, many students rely on student loans to finance their studies. However, managing multiple loans can be overwhelming and confusing. If you find yourself juggling multiple student loans with different interest rates and repayment terms, it might be worth considering student loan consolidation. But is it the right choice for you?

Student loan consolidation involves combining multiple federal or private student loans into a single loan with a new interest rate and repayment term. The primary goal of consolidation is to simplify loan repayment and potentially lower your monthly payments. However, before making a decision, it's crucial to understand the benefits and drawbacks of consolidation.

The Benefits of Student Loan Consolidation

Streamlined Repayment: Consolidating your student loans simplifies the repayment process by merging multiple loans into one. Instead of making separate payments to various lenders, you'll have a single monthly payment, which can be more manageable and less confusing.

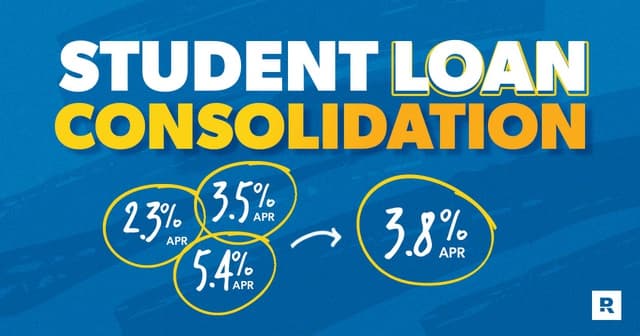

Potential for Lower Interest Rates: When consolidating federal student loans, the new interest rate is determined by taking the weighted average of your existing loans' interest rates and rounding it up to the nearest eighth of a percentage point. This means that if you have loans with high-interest rates, consolidation could potentially result in a lower overall interest rate, saving you money over the life of the loan.

Extended Repayment Term: Consolidation offers the opportunity to extend the repayment term, which can reduce your monthly payments. This can be particularly beneficial if you're struggling to meet your current payment obligations.

Fixed Interest Rate: Federal loan consolidations offer a fixed interest rate, which means your interest rate won't change over the life of the loan. This can provide stability and protect you from future interest rate increases.

Drawbacks to Consider

Loss of Benefits: Consolidating federal loans may result in the loss of certain benefits and protections offered by the original loans. For example, if you consolidate your federal loans, you will no longer be eligible for income-driven repayment plans, loan forgiveness programs, or interest rate discounts specific to the original loans.

Potential Increase in Total Interest Paid: While consolidation can provide a lower interest rate in some cases, extending the repayment term can result in paying more interest over the life of the loan. It's important to weigh the potential monthly savings against the total interest you would pay in the long run.

Eligibility Restrictions: Not all student loans are eligible for consolidation. Private student loans, for instance, cannot be consolidated with federal loans. Additionally, certain federal loan forgiveness programs may have specific requirements that could be impacted by consolidation.

Making an Informed Decision

Now that you are aware of the potential benefits and drawbacks, how do you decide whether student loan consolidation is the right choice for you? Here are a few factors to consider:

Evaluate your current loans: Examine the interest rates, repayment terms, and any benefits or protections associated with your existing loans. Determine whether consolidation would simplify your repayment process and potentially save you money.

Assess your financial situation: Consider your current financial circumstances, including your income, expenses, and long-term financial goals. If you're struggling to meet your monthly payments or need more flexibility in your budget, consolidation may be worth considering.

Research and compare lenders: If you decide to consolidate your loans, research different lenders and their consolidation options. Compare interest rates, repayment terms, and any additional fees or benefits they offer. Make sure to choose a reputable lender with favorable terms.

Consult with a financial advisor: If you're unsure about whether consolidation is right for you or need assistance in analyzing your financial situation, consider consulting with a financial advisor who specializes in student loans. They can provide personalized advice based on your unique circumstances.

Conclusion

Consolidating your student loans can simplify your repayment process and potentially reduce your monthly payments. It offers benefits such as a streamlined repayment, potentially lower interest rates, and extended repayment terms. However, it's essential to weigh these advantages against potential drawbacks, such as the loss of benefits and the potential increase in total interest paid.

Ultimately, the decision to consolidate your student loans should be based on a careful evaluation of your current loans, financial situation, and long-term goals. Take the time to research and understand the terms and conditions of consolidation options before making a decision. Consulting with a financial advisor can also provide valuable guidance. With thorough consideration, you can make an informed decision that aligns with your financial needs and objectives.

{kind=link}